The financial services industry has created meaningful, though still limited, opportunities for legal cannabis businesses in recent years. Despite the rapid growth of state-legal markets, cannabis remains classified as a Schedule I substance under the Controlled Substances Act. This classification continues to create a fundamental tension: activities legal at the state level remain federally prohibited, placing banks and credit unions in a complex compliance environment.

Over the past decade, financial institutions have gradually developed frameworks to manage this risk. Guidance from the Financial Crimes Enforcement Network, along with the now-rescinded Cole Memorandum, helped set expectations for monitoring, reporting, and risk management. These frameworks have led to specialized compliance programs and third-party technology providers that enhance customer due diligence (CDD), transaction monitoring, and ongoing risk assessment. As a result, more institutions have cautiously entered the cannabis banking space, primarily on the depository side.

However, lending remains the industry’s most significant gap.

Unlike deposit accounts, which can be tightly monitored and exited if risk thresholds are exceeded, credit products introduce longer-term exposure and balance sheet risk. Cannabis businesses often lack access to traditional financing, forcing them to rely on private lenders, sale-leasebacks, or high-interest debt structures. For banks, the absence of federal protections means that issuing loans to cannabis operators could trigger regulatory scrutiny, reputational risk, or even enforcement actions.

This is where the CLIMB Act has emerged as a pivotal development as of early 2026.

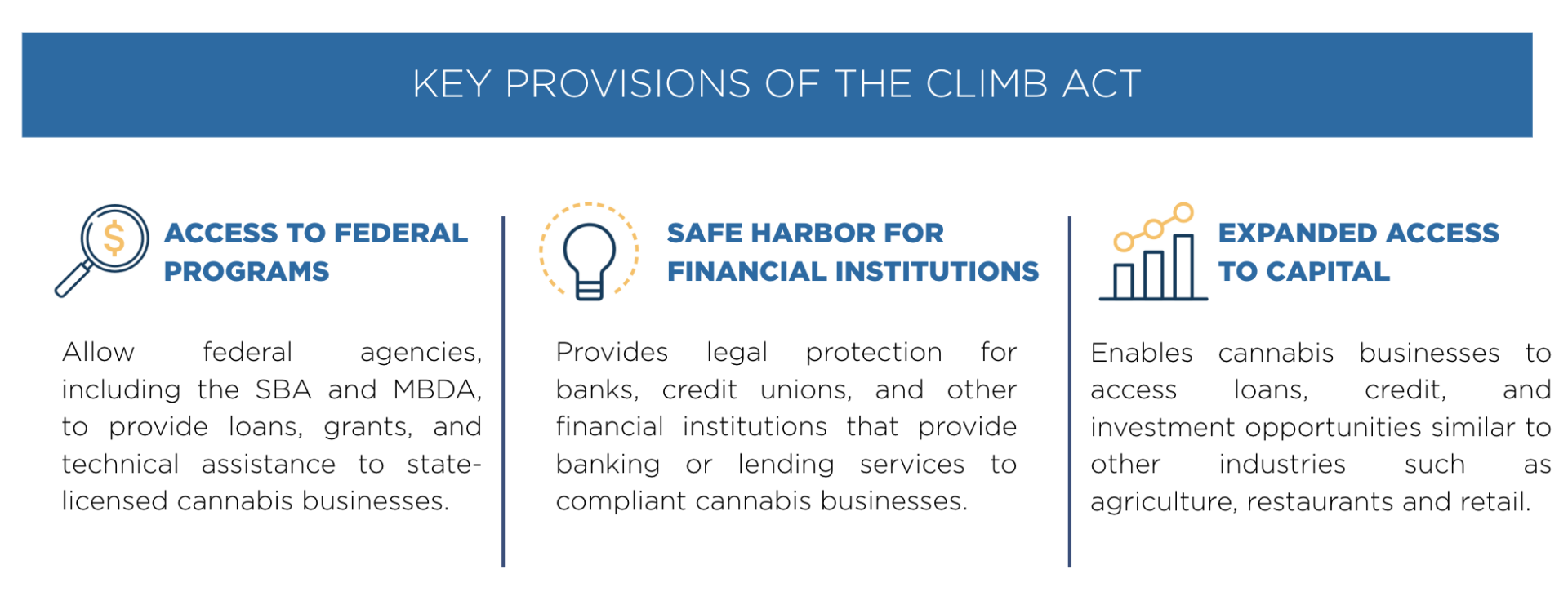

The CLIMB Act is designed to address one of the most persistent inequities in the cannabis industry: access to capital. Specifically, the legislation would:

Importantly, the CLIMB Act goes beyond banking. It represents an effort to normalize cannabis as a legitimate sector within the broader U.S. economy. By unlocking federal lending programs and reducing institutional risk, the bill could significantly reshape how capital flows into the industry.

Troy Carter has been a leading advocate for the legislation. In public statements, he has emphasized the importance of economic inclusion, highlighting how access to capital can help communities disproportionately impacted by past cannabis criminalization participate in, and benefit from, the legal market.

Although the CLIMB Act has not yet been enacted, its momentum reflects a broader shift in federal dialogue on cannabis policy. It also complements other legislative efforts to reform banking, signaling growing recognition that the current system creates inefficiencies and inequities.

For companies like NCS Analytics, these developments are particularly significant.

NCS Analytics operates at the intersection of compliance, risk, and financial transparency in the cannabis industry. Its solutions are designed to help financial institutions and lenders better understand the operational and financial health of cannabis businesses- an essential capability in a sector where standardized financial reporting is often lacking. Products like NCS Thea translate fragmented operational data into actionable risk insights, enabling more informed credit decisions.

Within the context of the CLIMB Act, platforms like NCS Analytics could play a critical role in accelerating adoption. Even with regulatory protections in place, financial institutions will still need robust tools to assess borrower risk, monitor performance, and ensure ongoing compliance. By providing a clearer “signal” from complex data, NCS Analytics helps bridge the trust gap that has historically limited cannabis lending.

If enacted, the CLIMB Act would not eliminate all challenges, but it would significantly reduce the barriers that have kept traditional lenders on the sidelines. Combined with advances in data analytics and risk modeling, this legislation could mark a turning point: transforming cannabis from a cash-heavy, capital-constrained industry into one with greater financial stability, transparency, and access to growth capital.

Ultimately, the convergence of policy reform and technological innovation may define the next phase of cannabis finance, one in which institutions are not only willing but also equipped to lend.

Read more about The CLIMB Act here: https://www.congress.gov/bill/117th-congress/house-bill/8200

Our team of experts collaborate and share insights to keep

high-risk industries safe and compliant.